Chakradhar Rangi

Chakradhar Rangi

Home

Posts

Projects

Publications

Contact

Notes

Light

Dark

Automatic

QuantFinance

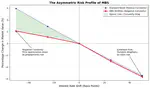

Quantifying Negative Convexity in Mortgage-Backed Securities

Developed a quantitative framework to model the cash flows and price sensitivity of Mortgage-Backed Securities (MBS). The primary focus is investigating the phenomenon of Negative Convexity—the asymmetric risk profile caused by the embedded homeowner prepayment option.

Code

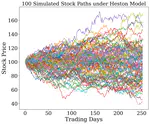

Erdos Institute Quant Finance Bootcamp

A series of mini-projects implementing Modern Portfolio Theory, volatility modeling, and risk-management strategies using Python and stochastic calculus.

Code

Certificate

Cite

×